The ERCOT Firm-Gas Overlap Problem

For hyperscalers pricing offtakes and infra funds valuing platforms: the ERCOT firm-gas pool that is both deliverable and committed is smaller than either filter suggests.

For hyperscalers · For infra funds · ercot · gas · interconnection · batch-zero · turbine-slots

Tafel Power · July 9, 2026 · 3 min read

Every discussion of ERCOT supply starts with the interconnection queue, and the queue is the most-cited and least-useful number in Texas power. It is a list of intentions filtered only by a study request, not a measure of what will be built. For firm gas, the resource AI loads actually need, the gap between the headline and the deliverable set is wide enough to change how a deal should be priced.

Three filters that barely overlap

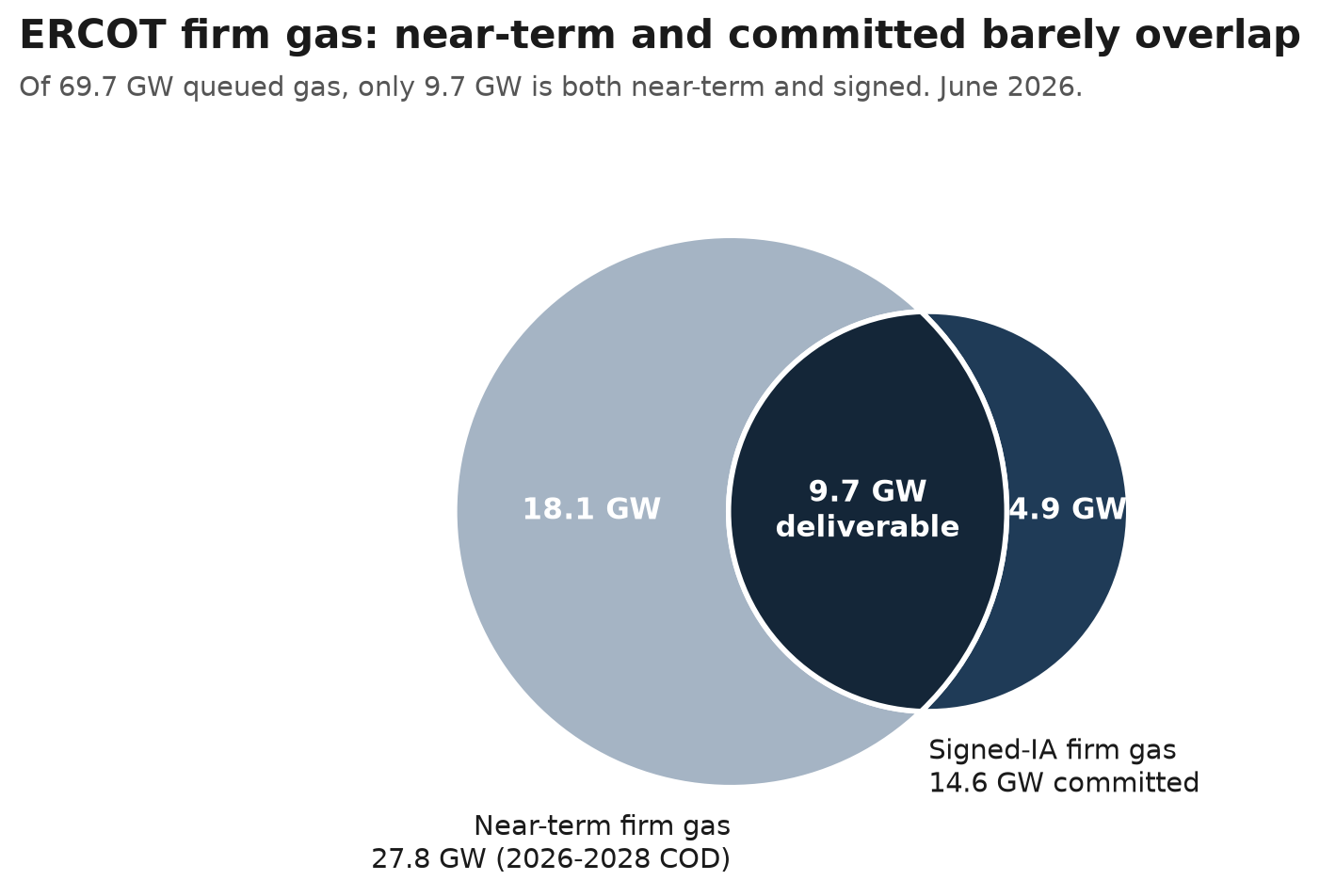

Total queued gas in the June 2026 GIS report is 69.7 GW. Apply a single filter and the number falls sharply. Filter to a 2026 to 2028 commercial operation date and it is 27.8 GW. Filter instead to a signed interconnection agreement and it is 14.6 GW.

The trap is assuming these are the same projects. They are not. Much of the signed capacity carries a 2029 to 2031 date. Most of the near-term capacity has cleared no interconnection agreement. The intersection, gas that is both committed and near-term, is only 9.7 GW. Of that 9.7 GW, about 0.9 GW is public-authority self-build, mostly LCRA, which no merchant offtaker can buy. Remove it and the merchant deliverable set is 8.8 GW.

Why 8.8 GW is the number that matters

8.8 GW is 13 percent of the gross gas queue. It is the realistic supply curve for firm capacity in ERCOT over the next three years, and it is thin enough to be personal. The set sits in roughly fifteen developers. When the deliverable inventory is that concentrated, firm power is priced by relationship and option value, not by the kind of clearing auction a market this small is unlikely to produce.

Two forces are about to tighten it further. PUCT Project 58481 will raise financial security requirements for large loads, which thins the unsigned majority of the near-term set. And even the committed 8.8 GW is gated upstream by turbine availability, where slot reservations and pricing are both moving against buyers.

What this changes for each buyer

Hyperscaler energy leads pricing offtakes in ERCOT. Secure options early against a named, countable set, rather than waiting for a clearing price that a market of roughly fifteen counterparties will not produce. The deliverable inventory for firm gas before 2029 is 8.8 GW, and it is contracted by relationship and option value, not by auction.

Infra funds underwriting large-load or gas platform acquisitions. The deliverable denominator is 8.8 GW, not 27.8 GW. A model built on the near-term figure is counting roughly 19 GW of unsigned projects that may never connect on schedule. Diligence the interconnection agreement and the turbine slot, not the queue position.

Developers holding firm-gas positions. Signed, near-term gas is the scarce asset. As PUCT 58481 raises financial security requirements and turbine slots tighten, the gap between a committed position and a speculative one widens, and the value concentrates in the committed position.

Methodology

Figures are drawn from the ERCOT June 2026 GIS Report (Large and Small Gen, projects with a Full Interconnection Study requested) and reconciled against that immutable source file before publication. "Signed IA" reflects the report's IA Signed field, corroborated by the GIM Study Phase field. Where the two disagree, the more conservative non-signed reading is used. Near-term means a developer-requested COD of 2026 to 2028, which skews optimistic and should be read as an upper bound. Merchant excludes cooperatives, municipal utilities, and public authorities. Figures reflect the June 2026 snapshot and may have changed since.

Because the 8.8 GW figure is derived from multiple filters applied to ERCOT GIS fields, it should be read as Tafel Power's filtered estimate of merchant, signed, near-term gas capacity, not as an ERCOT-published category.

All data compiled by Tafel Power from public sources. Framing informed by the firm's transaction advisory work in ERCOT and cross-ISO markets.

For discussions on ERCOT and cross-ISO power transactions, large-load diligence, or AI infrastructure power strategy: kris@tafelpower.com

More from Insights

Batch Zero's Interim Framework and the $50,000 per MW Default

For developers · ercot · batch-zero · puct

July 8, 2026 · 2 min read

For developers with queue positions and offtakers structuring around them: what the new $50,000 per MW default financial security means for deal math.

The ERCOT Queue by Fuel and IA Status

ercot · interconnection · reference-data

July 5, 2026 · 1 min read

June 2026 snapshot. 434 GW in queue. 134 GW with signed interconnection agreements. Breakdown by technology.