Markets

Firm gas across the seven US ISOs, reconciled from each market's own interconnection queue and the federal generator inventory.

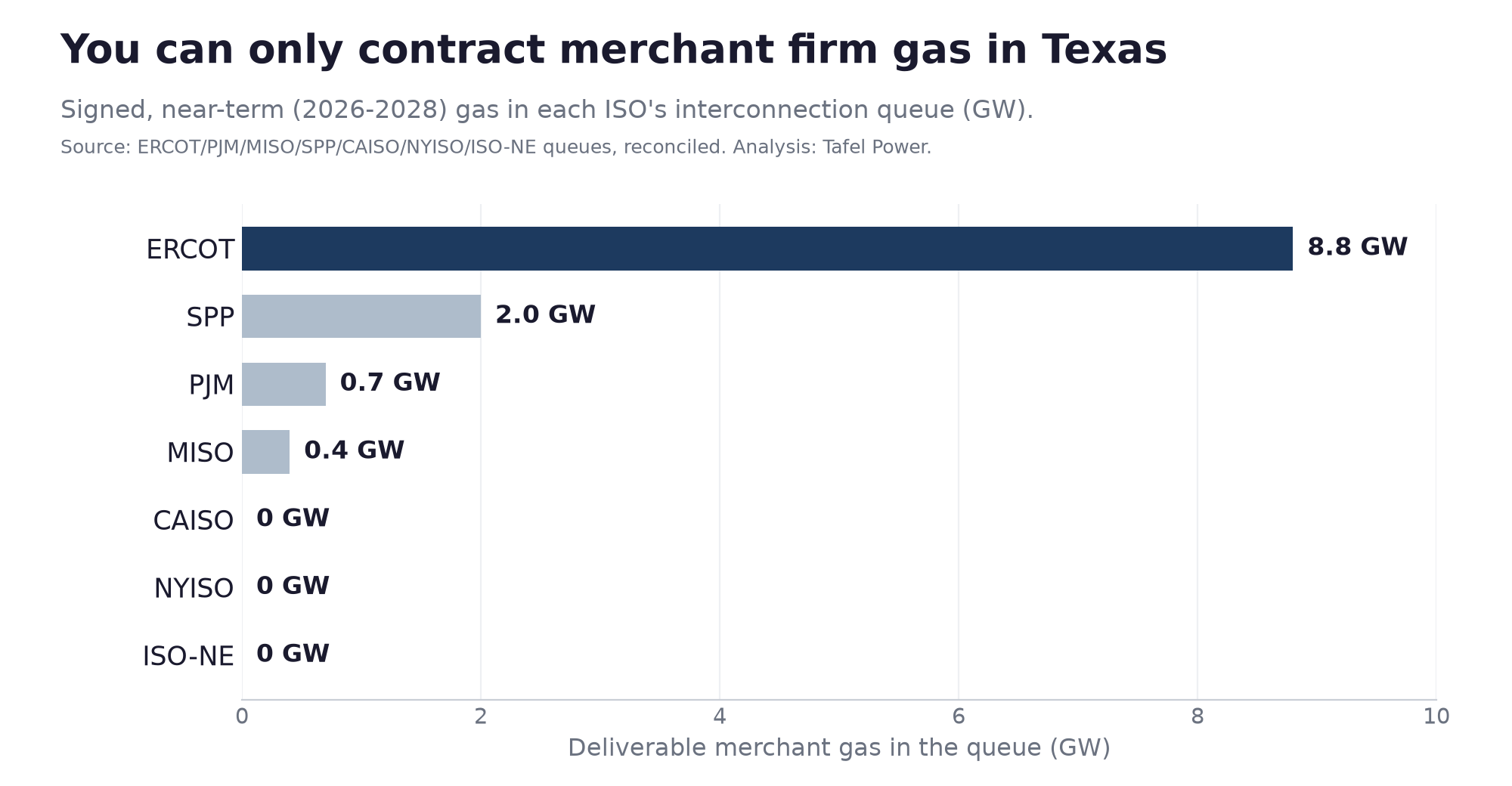

The same question runs through every market: how much firm gas can a large load actually contract, and how. The answer splits on market structure. In energy-only, merchant ERCOT, the interconnection queue is a real supply signal and holds 8.8 GW of deliverable gas. In the regulated markets, the queue is nearly empty of new gas because the utilities build through resource plans, not merchant queue positions.

Read the interconnection queue in Texas. Read the utility everywhere else.

| Market | Deliverable gas | Existing gas | Planned gas | Structure |

|---|---|---|---|---|

| ERCOT | 8.8 GW | 60 GW | 3.5 GW | Energy-only, merchant |

| SPP | 2 GW | 33 GW | 6.9 GW | RTO, largely regulated utilities |

| PJM | 0.7 GW | 95 GW | 5.8 GW | Capacity market, mixed merchant and regulated |

| MISO | 0.4 GW | 74 GW | 15.1 GW | Regulated, vertically integrated utilities |

| CAISO | ~0 GW | 29 GW | ~0 GW | Regulated, decarbonizing |

| NYISO | ~0 GW | 24 GW | ~0 GW | Regulated, decarbonizing |

| ISO-NE | ~0 GW | 15 GW | ~0 GW | Regulated, constrained |

One market sits outside the ISOs and dwarfs them: the regulated Southeast (Georgia Power, TVA, and their peers) holds roughly 181 GW of existing gas, more than any organized market. That capacity is utility-owned, so a data center reaches it through the utility on a regulated timeline, not through a merchant queue. It is why Georgia is one of the hottest data-center destinations, and it does not appear in any queue.

Deliverable gas is Tafel Power's filtered estimate from each ISO's own queue (signed interconnection agreement, in service 2026 to 2028, merchant), not an ISO-published category. Existing and planned gas are from EIA-860M. Figures reflect mid-2026 snapshots and may have changed since.

ERCOT (Texas)

By far the deepest merchant firm-gas queue in the US, and the only one at real scale.

PJM Interconnection

The world's largest data-center market, and almost no new gas in the queue.

MISO

An empty-looking queue over the market building the most new gas in America.

SPP (Southwest Power Pool)

The overlooked second-largest merchant firm-gas queue, in Oklahoma and the Texas Panhandle.

CAISO (California)

A large gas fleet, and effectively no new gas being built.

NYISO (New York)

No gas in the interconnection queue at all.

ISO-NE (New England)

The gas in the queue is all legacy plants. Nothing new is coming.